| W.I.L. Home Page | Finance Digest Home |

| Sign Up | Offshore News Digest Home |

THE IRONY OF COMPLACENCY

So far, so good, for an unbalanced world the sky has yet to fall. And the longer a lopsided global economy continues to chug along with impunity, the more the broad consensus of opinion becomes convinced that this is a sustainable outcome. This increasingly complacent mindset may be about to meet its toughest challenge: A likely turn in the liquidity cycle appears to be on a collision course with ever-widening global imbalances. This could well be a lethal combination that triggers the long-awaited capitulation of the American consumer.

With the benefit of hindsight, the hows and whys of a benign outcome for the world economy in 2005 are crystal-clear. Basically, it was another year of follow the leader, as a U.S.-centric world continued to draw sustenance from the seemingly unflappable American consumer. Sure, there were a number of other factors that came into play elsewhere around the world namely, the apparent healing of the Japanese economy, an improvement in Euroland late in the year, and the ongoing boom in China. But suffice it to say, were it not for another year of solid support from U.S. consumer demand our latest estimates put real consumption growth at an impressive 3.5% in 2005 the rest of a largely externally dependent world would have been in big trouble.

What did it take for the American consumer to deliver yet again? With Americas internal income-generating capacity continuing to lag, U.S. consumers once again tapped the home equity till to draw support from the Asset Economy. According to Federal Reserve estimates, equity extraction by U.S. households topped $600 billion in 2005 more than enough to compensate for the shortfall of earned labor income. The personal saving rate fell deeper into negative territory that at any point since 1933, and outstanding household sector indebtedness as well as debt service burdens hit new record highs.

So much for what happened in 2005. The big question for the outlook and quite possibly the most important macro issue for world financial markets in 2006 is whether the American consumer can keep on delivering. My answer is an unequivocal no. Three factors lead to me to this conclusion, the first being the distinct likelihood that a shortfall in internal labor income generation persists. Second, I believe that asset effects will be far less supportive to the American consumer in 2006 than has been the case in recent years. Third, in an environment of subpar income generation, in conjunction with diminished wealth effects from the Asset Economy, the saving-short, overly indebted American consumer will instantly become more vulnerable to ever-present shocks.

Of those three factors, the asset effect is most likely to be the swing factor for the U.S. consumption outlook. This is precisely where the liquidity cycle comes into play. In my view, the froth in asset markets first equities in the late 1990s and, more recently, property is a direct by-product of a powerful surge in global liquidity. Courtesy of central bank policy normalization led by Americas Federal Reserve in conjunction with an important shift in the mix of global saving, there is good reason to look for a much slower flow from the global liquidity spigot in 2006. Experience tells us it is usually unwise to bet against the American consumer. While I think there are compelling reasons to go against the grain in 2006, I do so with great trepidation.

Excess domestic liquidity is the high-octane fuel of the Asset Economy and the consumer-led growth dynamic it fosters. Excess global liquidity is also responsible for the funding of Americas massive current-account deficit. Yet as the liquidity cycle now turns, the rules of engagement in the Asset Economy are likely to meet their sternest challenge. That is a big deal for the income-short U.S. consumer, leaving households with little choice other than to cut back discretionary spending. From the start, that has been the only real option for meaningful progress on the road to global rebalancing. The irony of complacency is about to strike again. The day of reckoning for an unbalanced world could be close at hand.

Link here.Between the lines of an optimitic/complacent 2006 outlook concensus.

I can think of no better way to kick off the year than by indulging in the total immersion of MacroVision. This two-day event internal workshops on the first day followed by interactive sessions with clients on the second day is designed to challenge every strand of our macro DNA. It is, first and foremost, a time-out from the blur of market and business demands. It provides us with an extended period for real-time debate with our colleagues and clients from around the world. It is a deep drill into the big issues that we believe will shape the global economy and world financial markets in the year ahead.

Over the years 15 of them when the event was limited to our worldwide team of market strategists and economists, and now five years that included some of our smartest clients we have spent a lot of time refining the drill. The good news is the process works. MacroVision has had a great track record of success in coming up with many a big call. There was global healing in 1998-99 and the great deflation scare in 2003. Last year, the conclusions were especially prescient well-contained inflation, no bond bubble, and the outperformance of European equities. Alas, there were also some important misses in 2005 especially, the dollar and oil prices. But the overall score for the calls coming out of last years MacroVision was about as high as it gets. That gave the assembled crowd pause for thought in peering into 2006. It is always tough for groupthink to put together two good years in a row.

I will not bore you with the details, but we follow a carefully structured process in driving the debate toward actionable investment conclusions. This year focused on the following themes: 1.) reforms, restructuring, and returns, 2.) consumer rebalancing, and 3.) global capital spending boom (or not). The magic of MacroVision occurs in what we call our synthesis sessions, where we bring the entire group together and compare and contrast the findings of the various workshops.

As I pondered my notes from this years MacroVision, I was particularly struck by the interplay between the consumer and the capex sessions. In general, the group was quite upbeat on the U.S. and global consumption outlook. There was little sympathy for my long-standing complaint about the excesses of the asset-dependent American consumer. Few seemed concerned that an income-short consumption dynamic might falter as the housing bubble now started to deflate. Actually, few seem concerned about the U.S. housing bubble, period. As one participant put it, American consumers will continue to buy its our way of life. As long as employment held up, went the argument, so would household spending. The group was nearly unanimous in believing that there was only modest downside to U.S. consumption, at worst. Furthermore, they argued, any such slippage would likely be offset by improved consumption in Japan, Europe, and China. The global consumer was given a clean bill of health for 2006 by the MacroVision consensus. I was truly the skeptic on the outside, looking in.

The second thematic conclusion of MacroVision 2006 was equally compelling that any global capex recovery was likely to be limited. The group felt strongly that businesses in most major economies would remain reluctant to increase productive capacity with, of course, the important exception of China. Instead, incremental growth in capital spending was generally expected to be earmarked toward replacement outlays, especially for short-lived IT equipment. Two possible exceptions were noted infrastructure especially water, roads, and transportation and energy exploration and refining. Private equity participants reinforced this view. Not one of our portfolio companies is thinking of adding significant capacity.

Putting these two conclusions together solid consumption and modest gains in capital spending unmasks what I believe could well be one of the more important inconsistencies of this years MacroVision. I have always viewed capex as a derived demand, highly sensitive to business expectations of future demand growth. If I am right and if the MacroVision consensus is correct on the consumption outlook then the derived-demand approach would argue for a far more vigorous capital spending outcome than the consensus is currently looking for. A sharp pickup in business fixed investment could have very important implications for the global macro call. For starters, it would mean a much stronger outcome for world GDP growth than most are expecting. Such an outcome could well lead to a sharper cyclical rise in inflation than the consensus is looking for. And that, of course, could turn the financial market climate from benign to malign. Such a scenario would also be strikingly reminiscent of the classic boom-bust cycles of yesteryear but with an important twist. The twist comes on the price front. Even in the context of a possible cyclical pickup in inflation, the peak inflation rate in this cycle is likely to be quite low possibly no higher than 3% in the industrial world.

As usual, we did a fair amount of polling of the groups macro expectations over the next year. As can be seen in the accompanying table, the consensus was focused on another Goldilocks-like outcome for the real economy and financial markets limited interest rate risk, a modest rise in the stock market, a slight weakening of the dollar, and another year of outperformance by emerging market equities; among the developed-world equity markets, Japan was the favorite, followed by the U.S. and Europe in that order. Like most of our macro polling these days, the group had a very autoregressive perception of the outlook extrapolating mainly on the basis of the latest trends. These are the polling results that always worry me the most momentum-driven scenarios that are not based on deep convictions. Should the story change for any reason, such a fickle consensus would undoubtedly head quickly for the exits a classic set-up for sharp and disruptive adjustments in financial markets.

The most intriguing conclusion was between the lines the implied risks of an upside surprise to global growth and a more cyclical outcome for the markets. My baseline call for global rebalancing has never felt lonelier. As we passed in the halls, many of the clients had a hard time making eye contact with me. Was it the height of complacency or well-founded optimism? We are about to find out.

Link here.HOME PRICES GET EVEN MORE OVERVALUED

Although many overheated U.S. housing markets lost steam during the third quarter of 2005, most still grew less affordable. That is according to the Local Market Monitor, a real-estate market research provider. hrough the third quarter of 2005, 79 of the 100 surveyed markets had gotten more expensive, relative to what LMM calculates as fair value. At the top of the list for overpriced cities was Santa Barbara, California at 86% overvalued. The average home there should cost $308,900, according to the LMM. Instead it sold for $573,100. The survey found that only 16 of the markets had gotten less expensive.

Overall, 37 markets were found to be severely overpriced, which meant that they were at least 15% more expensive than they should be, and only 6 were underpriced by 15% or more. 57 were deemd to be farily priced. While the slowdown in price increases seem to indicate the market has peaked, some regions, especially in the red-hot Sunshine State, continue to experience accelerating home prices. These included Naples, Florida where prices increased 32% in the 12 months through the end of the third quarter. That is after more modest increases of 18% in 2004 and 9% in 2003.

Link here.Business 2.0s list of dumbest moments in real estate in 2005.

#1.) Bubble Trouble, Grand Prize Winner, Dumbest Moment of 2005: If you grew up in Danvers, and you remember it as the spooky place on the hill, it might not be the right place to live. William McLaughlin, an executive with AvalonBay Communities, which is converting boarded-up Massachusetts mental institution Danvers State Hospital into a 497-unit complex of high-end apartments and condos. That sound you hear? Not the ghosts of mental patients, but loud hissing from the wildly inflated housing bubble, which tops our list this year with seven priceless moments of real estate insanity. First up: the nuthouse-to-yuppie-house trend currently sweeping North America, with such conversions also planned in Detroit, New York, Vancouver, and Columbia, S.C., where the centerpiece of the development is an original brick building with the word asylum chiseled into the facade.

#30.) Better get your offer in quick rumor has it, Kate Moss is very interested. A house in the Shepherds Bush area of London measuring less than 10 feet across at its widest goes on the market for $933,000. Listing agent Winkworths describes the anorexic structure asqutterly amazing and almost certainly unique.

#90.) See? Our plan to turn it into a bastion of American-style capitalism is working just fine. Before, in Iraq, the houses were cheap. Now the houses are expensive, but the lives are cheap. A real estate agent in Baghdad, about the red-hot market in the Iraqi capital, where prices have soared as much as 1,000% in the past three years. The increases are fueled by foreign investment, pent-up demand after Saddam Husseins strict property regulations, and even reinvested gains from looting.

#100.) Bubble? What bubble? Oh that bubble. In May an Experian-Gallup national survey finds that 65% of Americans have not heard anything about a possible housing bubble. Another 12% have heard only a little. Indeed, 70% expect home prices to keep rising, while only 5% think they will slip. However, when the facets of a housing bubble are described to them, about 40% go on to say that the scenario is likely to occur in their area in the next three years.

Link here.Economists see housing bubble deflating.

It is not the end of the world just the first signs that the housing bubble is beginning to deflate. That is the verdict economists delivered on the data that show an unexpectedly steep slump in the sales of existing homes in December despite a decline in mortgage lending rates that might have helped cushion such a decline. The National Association of Realtors reported sales of previously owned homes slid 5.7% in December over November levels, with about 6.6 million properties changing hands compared to 7 million in November 2005.

The market had been braced for a decline, but not of this magnitude. More striking still, it is the third-straight month that the volume of real estate transactions has fallen since peaking at 7.35 million units last June. Meanwhile, the median value of those homes has now fallen for two months running after hitting its recent high in August.

In a note fired off to clients, Ian Shepherdson, chief U.S. economist for High Frequency Economics, warned that this is just the start. We expect price increases to slow much further, dragging down expectations for future price gains and therefore raising real mortgage rates, Stepherdson cautioned. This will be the trigger for a serious collapse in home sales later this week. The housing market is a bubble, and it will burst.

We are expecting that consumers are going to be less able to draw on the equity in their homes, so job creation and income growth will take over as the primary drivers of spending, said Gary Thayer, chief economist at A.G. Edwards & Sons.

Link here. Trouble on the Home Front link.NYC Mayor: Housing market dramatically slowing.

New York City Mayor Michael Bloomberg last week said the real estate market was slowing dramatically and only a miracle could stop soaring mortgage rates from eating into housing prices. Consumers are definitely feeling the pinch of higher mortgage lending rates and are not quite as eager to snap up a new home especially at time when house prices in the Big Apple are near record-highs, the Republican mayor said in his weekly radio show. The real estate market is slowing down dramatically and were going to have a problem down the road, Bloomberg said. If people who want to sell their houses have to wait a longer time before someone comes along and buys it, it would be a miracle if prices didnt start to go down, he said.

The most recent data compiled by Prudential Douglas Elliman show the volume of sales of Manhattan apartments dropped. The survey also showed the number of for-sale units piled up in the last quarter of 2005, while buyers took longer to commit to a purchase although prices have not yet taken much of a hit as a result. Bloomberg, who won a second term in office in November by a landslide, said property taxes were on the rise, but were not climbing as fast as the values of the properties themselves, as state laws limit how much taxes can rise.

Link here.Name a 5-letter word that starts with P.

The big picture in the housing market got a bit clearer on Wednesday. Here is some of what we know. 1.) Existing home sales declined 5.7% in December, the third consecutive monthly decline in other words, homes sales fell during the entire fourth quarter of 2005. 2.) The monthly supply of existing homes for sale in 2005 increased in all but two months of the year; by December that supply had reached a multi-year high. 3.) Mortgage applications were lower the second half of 2005, falling 16 percent from a 12-month high reached in June (Bloomberg). Mortgage refinancings took an even more severe hit, falling 45% from the yearly high in June.

All that said, there is one more noteworthy statistic: Home sales still managed to exceed 7 million in 2005, an all-time record. Two things appear obvious: 1.) The demand for homes was voracious in the first half of the year but dropped precipitously in the second half; 2.) The supply of homes increased steadily all year long, to the point that sales are down three months in a row. So the rocket science question of the day is: When supply is rising, demand is falling, and sales head down which 5-letter word that begins with a p has to give? There is more to say about price in the housing market, its relationship to the economy, and to the entire debt bubble that hangs over the financial system.

Link here.McCains having trouble selling mansion.

Sen. John McCain is testing the declining real estate market as he tries to sell his recently price-reduced $3.75 million Phoenix mansion. The 11,000 square foot estate, with its 9 bedrooms and 8 bathrooms and 8 surveillance cameras has been on the market for three months. Only six prospective buyers have checked it out, the Arizona Republic says. That led to a half-million-dollar price cut. A year ago, there were 145 homes priced at $500,000 or more for sale in Phoenix. Now, there are 1,341. Houses were selling in days last year, but now, it is taking an average of six weeks. McCain and his wife, Cindy, who grew up in the house, want to downsize.

Link here.AS ECONOMY THRIVED UNDER GREENSPAN, SO DID DEBT

Millions of Americans who have prospered during Alan Greenspans 18 years as chairman of the Federal Reserve. They lived through nearly two decades of generally stable economic growth with low inflation, low unemployment and modest interest rates. Under Greenspans watch, the economy thrived despite stock market crashes, international financial crises, terrorist attacks, wars and other shocks. No wonder, as Greenspan prepares to retire next week, economists have lauded him as the greatest central banker ever.

Still, his legacy will be judged not just by his record at the Fed, but also by the economy he bequeaths. And when he leaves office January 31, Greenspan leaves a nation awash in debt record household debt and a record trade gap. Many analysts say his low interest rate policies contributed to these huge imbalances, which threaten the economy he nurtured. The jury is out on his legacy in large part because of the debt and the trade deficit, said Stephen S. Roach, chief economist at Morgan Stanley. You will not be able to truly judge his accomplishments until we see how this plays out in the post-Greenspan era.

Greenspan and his Fed colleagues agree that part of the growth in household debt and the trade gap is the side effect of policies that helped steady the U.S. economy after the stock bubble burst in 2000. The Feds low interest rates encouraged consumers to borrow and spend on houses, autos and other goods, spurring economic growth for several years when businesses were cutting jobs and reluctant to invest. And it was no surprise that consumers spent much of their borrowed money on imports, causing the trade deficit to swell. But in the view of central bank policymakers, the alternative would have been worse a longer and more painful downturn.

Greenspans Fed did not do it alone, economists agree. Other factors helped fuel the borrowing binge, including global financial trends that have helped keep mortgage rates low and prompted lenders to extend more credit to more people. The result is a prosperity built on borrowing, say many economists, pointing to a string of recent records and firsts: (1) U.S. household debt hit a record $11.4 trillion in last years third quarter, after shooting up at the fastest rate since 1985. (2) U.S. households spent a record 13.75% of their after-tax, or disposable, income on servicing their debts in the third quarter. (3) The trade deficit for last year is estimated to have swollen to another record high, above $700 billion, increasing Americas indebtedness to foreigners.

The economys increasing reliance on unprecedented levels of debt is clearly unsustainable and extremely troubling, said Charles W. McMillion, chief economist with MBG Information Services, a financial analysis firm. The only serious questions are when and how will current imbalances be addressed and what will be the consequences. The Fed chairman told Congress in June: I think weve learned very early on in economic history that debt in modest quantities does enhance the rate of growth of an economy and does create higher standards of living, but in excess, creates very serious problems.

Greenspan did not define excess, but economists see troubling possibilities: A sudden reversal in housing prices could trigger a recession if consumers cut back on spending and households have trouble paying their mortgages. The trade gap could swell to a point that forces a sharp fall in the dollar and surge in interest rates, also causing a recession. Even without a crisis, the debt load will weigh on the economy simply because of the interest to be paid on it, which leaves less money to spend on other things and prevents living standards from rising as fast as they would otherwise, some analysts believe.

Link here.LIQUIDITY FIRE TRAP?

Following a near melt-up in share prices at the beginning of this month, markets have suddenly become unstuck. Rattled in part by disappointing results from the likes of Intel, GE and Citigroup, as well as jitters over Iran and sharply higher oil prices, many investors are looking to take money off the table and head for safety. Unfortunately, there are signs that some exits are becoming blocked. What that means is, those looking to cash out in the months ahead may soon discover that they are trapped with little or no way out.

Take last weeks debacle in Japan. When word of an investigation at former high-flyer Livedoor unleashed a wave of selling by small investors, volume surged. That forced officials at the Tokyo Stock Exchange to halt trading early because of capacity constraints, despite the fact that the internet companys sub-$10 billion value paled in comparison to the $4 trillion capitalization of the overall market. Then there are the problems in Germany. Since last month, two real estate mutual funds, with assets totaling $8 billion between them, have been forced to temporarily shut their doors to prevent runs by nervous investors. Under that countrys rules, funds investing in property need only hold 5% of their assets in cash no doubt a problem if too many decide, as they have recently, to bail out all at once.

Doors are closing elsewhere, too. According to a recent report, one $12 billion U.S. hedge fund among others recently started enforcing longstanding policies designed to penalize investors seeking to withdraw more than a predetermined amount at one time. The reason for the sudden intransigence? Fears that investor nervousness over poor performance will spur a mass exodus. Several hedge fund managers are using a loophole in new rules requiring hedge funds to register with the SEC funds with lockups greater than two years to be exempt from registration as an excuse to tie up investors assets for long periods of time.

Combine all this with the widespread and wide-eyed rush to invest in private equity funds, over-the-counter derivatives, thinly-traded securities, and a host of other illiquid assets, and it is not hard to see how numerous investors have struck something of a Faustian bargain. That is, they have accepted the prospect of marginally higher returns in exchange for much greater risk and increasingly limited access to their money. But what might once have been viewed as nothing more than a temporary inconvenience may turn out to be something else: a liquidity fire trap. Let us hope no one gets too burned in the rush for the exits.

Link here.GERMAN LEADERS WAKE UP TO SHRINKING POPULATION

Are Germans an endangered species? Stunning as it may seem, a steep decline in the German population since 1972 and fears the trend will gain pace have led demographers to warn of unsettling consequences. The number of Germans has declined by 3.2 million the population of Berlin over the last 30 years but demographers concerns have mostly been ignored until now in a country scarred by the Nazis nefarious procreation pressures. German leaders have now lifted the birth rate to the top of the political agenda for the first time since the Nazi era, and the two ruling parties are trying to outdo each other with pro-family measures. Harald Michel, managing director of the Institute for Applied Demography, fears the German population could shrink from 75 million to 50 million by 2050 and further after that.

Germans have long had one of the lowest birth rates in the EU at 1.3 children per woman far below the replacement rate of 2.1 needed to keep the population stable and about half the rate of 40 years ago. More than 30% of east and west Germans born from 1960 to 1967 will remain childless. Among Germans with higher education, the childless rate is even higher at 38%. Each generation is being reduced by about a third, said Norbert Walter, chief economist at Deutsche Bank. The consequences are foreseeable, he added, referring to the financial havoc a shrinking population is causing in areas ranging from the increasingly underfunded state pension system to weak consumer spending and sagging property values. I think its an exaggeration to talk about Germans becoming extinct. But when a country that once had more than 80 million people ends up with only 60 million at some point down the road, well, that will be a completely different country then.

The silent shrinking has so far been masked by immigrants. But Germanys anemic economy is no longer a magnet and the total population, which includes 7 million foreigners, has actually declined in recent years from a peak of 82,536,680 in 2002 to 82,500,849 in 2004. Low birth rates plague other nations like Italy, Russia and Japan where the average number of children a woman bears in her lifetime fell to a record low in 2005. But demographers say Germany is worse off because the problem has been ignored for so long. In other leading industrial nations like the U.S., Britain and France, birth rates are much closer to the replacement rate.

Link here.Japan: A cold snap in stocks and sex?

Over the past month, people in Japan have written the book on how to survive the Winter of Our Discontent and we are not just talking about the raging blizzard that recently left the countrys seacoast under 13 feet of snow. It appears that the coldest temperatures in decades goes beyond the mercury reading on the thermometer, to include the dating scene among Japans eligible singles. According to experts on the subject, two words now confront the female population: Men Overboard, as court-ship has foundered in glacial seas.

A January 10 Japanese Times article puts it this way: Things in this country arent so hot, literally, [as] a Renai Ken-o-Sho or Out of Love Epidemic eats away at the hearts and minds of Japanese men, making them reluctant to get close and committed to serious partnerships. The high costs of this anti-amore affliction include plunging birth rates, an extreme lack of relationship-security, and the lowest number of loving couples in the last decade. But while the booing of wooing by Japans bachelors may be baffling to some, it is a perfect example of what happens to a society when the collective psychology turns cold.

On this, the Elliott Wave Principle reveals the many manifestations of a downtrend in mass social mood, including an overall shift in the mindset of the public from friskiness to frigidness, affection to alienation, intimacy to isolation; a decline in birth rates and disfavor of monogamy. Ring any bells? The truth is, while a slide in social mood makes mankind less frisky in its mating habits, it also makes mankind less risky in its stock market habits. To wit, investors go from courageous to cautious, speculative to specific right before ones very eyes.

And on January 18, the Japanese market offered living proof that such a shift had occurred when the Tokyo Stock Exchange Mothers Index plunged nearly 300 points in its biggest one-day slide since May of 2004. To put things into perspective, between September 29 and January 18, the Mothers Index soared a whopping 60%. Then, in just three market days, prices erased 25% of that rise. Bear in mind, the fundamental experts blamed the nosedive on the alleged Livedoor scandal, the details of which hit the press that morning. But we urge you to think harder than that.

The Mothers Index includes a very small number of start-up and emerging stocks, all in the early stage of development. Their appeal is NOT in actual earnings, but expected earnings and the potential for growth. Meaning: the share price of these stocks depends on FAITH not FACTS. By no means is it scandal that caused investors to flee from the Mothers Index. It is their loss of confidence that weathering such a scandal will ultimately reap higher rewards in the end. And that is a direct result of a downturn in mass social mood.

Elliott Wave International.THE UNVARNISHED, UNADULTERATED, UNSWEETENED, UNSULLIED STORY

OK today, we give it to you straight. No metaphors. No jokes. No irony. No sarcasm. Today, you are going to get the story unvarnished, unadulterated, unsweetened, unsullied like a shot of Old Overholt Pennsylvania rye whiskey without the branch water oh, never mind. There are four macro-trends, all related, and all affecting the world at the same time:

The world is running out of cheap oil. Yes, there will always be energy, but it will be harder and more expensive to get. The entire worlds oil production is expected to peak out in a year or two. Cutbacks in supply could not come at a worse time; more people want more oil than ever before. Currently, the average Chinese consumes less than 1/10th as much energy as the average American. Wait until they consume just half as much! $3 for gasoline now seems certain. In a few years, it will seem cheap.

The worlds wealth is shifting to the East. GM, recently Americas largest company, is worth $12 billion. Put it together with Ford and they are still worth less than half of Honda, and less than a fifth of Toyota, with a market cap of $172 billion. Over the next 10-20 years, Asian markets, including Japan, could have 25% to possibly 50% of the world market cap, from 14% currently. A friend of ours just returned from Shanghai: Theres so much money so much energy so much life. It must be like New York was in 1910 or 1920. Globalization has wrought competition. Now, faster, lighter competitors in the East are eating Americas lunch and kicking its derriere just as New Yorkers did to Londoners a century ago.

The U.S. Empire is peaking out. From the get-go, the U.S. Empire has always been a slippery grog of Wilsonian moonshine and Custerian military hooch. Those two intoxications have come together in an explosive and disgusting concoction: The Iraq campaign a war that is both strategically incompetent and operationally ruinous. But what is really sapping the empires strength is money, or more precisely, a lack of it. Americans would rather have granite countertops and free pills than have a costly empire. They cannot afford both not with globalization marking down the American workingmans daily rate. So, their debts rise. Drenched in easy money, a decadent mildew spreads. Get it while you can, say the corporate hustlers, lifestyle gurus, and money shufflers. Wall Street, for example, is enjoying another year of record bonuses. Henry Paulson, Jr., CEO of Goldman, will get $38 million.

With the decline of the empire comes the decline of the empires money the dollar. When the dollar was cut loose from gold on August 15, 1971, thinking men posed themselves a question: How long would the dollar last? The answer is still unknown, but the day of its demise gets closer all the time. Yesterday, the euro jumped above $1.23. Gold headed for $560. This experimental drama with paper money as the lead role has a few acts to go, but we all know how it will end. The dollar will go down; it will fall like Macbeth at Dunsinane.

There is also an important cyclical trend to consider. Markets go up and down, even while the great macro-trends work their wills and their ways. A major expansion of credit, and an increase in asset prices, began in the early 1980s. In terms of real money (gold), prices for stocks, bonds, and real estate all over the world rose. That inflation of asset prices came to an end in July of 1999. Since then, gold has gone up against almost all asset classes. The trend has just begun. And since most people only look at prices in nominal, local currency terms, few people have noticed. But asset prices are deflating. In terms of real money (gold), stocks, bonds and property are going down.

This, too, could not come at a worse time. U.S. credit market debt is more than twice what it was when the expansion began in 1980; it has gone from 130% of GDP to more than 300%. That debt especially mortgage debt rests on inflated asset values. When asset prices go down, so will the debt itself. And then, the struggling householder, the poor yeoman consumer, the purchasing prole, what will he do? Pinched between the Scylla of debt and the Charybdis of declining real, spendable income with all the costs, illusions of a decaying empire to sustain, with his dollars losing value (and his Fed chief dropping them from helicopters) pumping $3 gasoline into his gas-guzzling land barge, and making monthly payments on a mortgage that towers over his house like the Washington Monument over a bums cardboard box what will the poor man do?

We almost think we know the answer. He will turn to the left. But that is another story for another day.

Link here.Let us see how our major trends are holding up

The days of cheap energy are over. Kuwait confessed that it has about half the oil it once claimed. And like a fat lady in the pastry section before a snowstorm, China is buying up oil reserves wherever it can find them in Nigeria, in Ecuador, and in Syria. Meanwhile, wealth leaks rapidly out of the West and into the East. The U.S. Empire loses ground against China and the rest of Asia, too. Its domestic economy grew only about a third as fast last year, and not half as well. China is growing, albeit in a reckless and dangerous way, by building more productive capacity. That is real growth growth that can add to its wealth. America, on the other hand, is growing by consuming its wealth, like a man who sells the family business in order to buy a beach condo. He seems richer. He feels richer. He gets a new girl friend and a tan. At least, he looks healthy and happy when he arrives in bankruptcy court.

The American economy heads into 2006 with a full head of steam, claimed the empires chief executive. Neither war, nor high oil prices, nor hurricanes could keep it from its rendezvous with destiny, he went on. He is surely right; but how much destiny does a decadent empire have? According to the LA Times, polls show that half the public thinks the economy is in bad shape and that Bush is doing a bad job of managing it. One survey showed that 30% of the population believes the U.S. is in a recession. And the bankruptcy figures show that for many people, the it might as well be in a slump. They do not seem to be able to make ends meet.

Oh Alan, Alan what have you done? You have lured a whole generation into a debt trap from which they cannot get out. Debt service, as a percentage of income, is at a record high. Even with Mom and Dad both working, family expenses exceed income. What can the lumpenhouseholders do but pray for a miracle, file for bankruptcy, or cut back even more? And what can your successor at the Fed do? The poor man is already checking out helicopters. He figures he might have to drop $100 bills from the air in order to keep Americas bubbles inflated. He is probably right. A credit expansion must be followed by a credit contraction.

Gold is still edging up toward $560 an ounce. The dollar fell yesterday. The latest experiment with paper money is beginning a new phase. It was relatively simple for a central bank to shepherd a paper money when it was rising against real money (gold). The bankers could simply print more of it. Everyone was happy. Now, we will see what happens when the paper money falls. Will investors be so ready to loan out dollars? Will they buy Treasuries at todays low yields? Will housing prices go up when yields rise? Without higher house prices, how will consumers continue consuming?

Alan Greenspan entered the Fed with room to maneuver, for Paul Volcker had broken the consumer price inflation of the 70s. Gold was going down. Consumer debt was less than half what it is today, while asset prices were low. And the esteem in which central banking was held was let us say moderate. All he had to do was to make money easy to get. But poor Ben Bernanke comes upon the scene with everything running against him. Money has been too easy for too long. People already have too much credit, too many debts, and too many expenses. But Bernanke battling a forest fire with a woodpile plans to give them more. We are already pulling up a comfy chair and buying popcorn. It will be fun to watch the show.

Link here.BAGGING TEXAS TEA, PART II

Last week, I cited Anadarko, Devon and Occidental as potential takeover candidates in the oil and gas industry. Allow me to provide a bit more detail. Anadarko Petroleum (NYSE: APC) is coming out of a period of restructuring. It has a new focus on long-lived resources and growth areas. I see this as both a benefit to shareholders and a big, fat lure to asset-hungry oil majors. Anadarkos long-term strategy focuses on unconventional oil and gas reserves in well-known, mature basins. Unconventional refers to reserves like tight gas and coal bed methane, as well as those reserves that require some sort of enhanced recovery process. The U.S. Geological Survey has identified over 1,000 trillion cubic feet of these unconventional gas-equivalent reserves still remaining in North America.

The second part of Anadarkos new strategy is to pursue growth through its expertise in both onshore and offshore exploration. The companys research division leads the industry in seismic imaging. Thanks largely to its exploration successes, Anadarko owns interests in 7 of 9 major discoveries in the Gulf of Mexico. As of October 2005, the company had 68 drilling rigs operating. During the third-quarter alone, Anadarko drilled 241 wells with a 99% success rate. Since Anadarkos proven reserves would increase the reserves of the average major oil company by nearly 20%, the company should be a compelling target for every one of the Majors. And Anadarkos assets will become even more valuable to a Major as the industrys cost of finding and replacing reserves steadily increases.

Anadarkos undeveloped regions are primarily in Canada, Alaska, and the lower 48 states. The company holds over 7 million undeveloped acres in prime oil and gas regions. All production and proven reserves aside, these land holdings alone make Anadarko an extremely attractive takeover prospect. In 2004, the company sold properties that did not fit with its new strategy. It used the proceeds to pay down $1.2 billion in long-term debt and buy back $1.3 billion in common stock. Now that Anadarko has both its exploration and financial houses in order, it is ripe for the picking. The stock currently trades around $105 per share, but Kurt Wulffs McDep Associates estimates Anadarkos net present value to be $140 per share.

Next up is Devon Energy (NYSE: DVN), one of the best values in oil and gas independents. Its strategy is to focus on low-risk exploration, while investing in select high-impact projects for future growth. Devon uses acquisitions to fuel its growth it acquired five companies from 1998 to 2003. Its last acquisition, Ocean Energy, made Devon the largest U.S. independent oil and gas producer. Devon is very active in North American fields, as well as the largest U.S.-based independent producer in Canada. Among all the independents, it is the largest gas producer in Texas, the 3rd largest gas producer in Wyoming, and the largest oil producer in New Mexico.

Devons current exploration inventory includes some very attractive offshore acreage. The offshore locations include 56 prospects in the Gulf of Mexico, 21 prospects in the offshore area of Brazil, including the Campos basin, and 20 prospects offshore of West Africa. In addition to those ready-to-drill prospects, Devon has large blocks of unexplored acreage in the most desirable offshore basins. I am surprised this company is still on the table at all. Devon would be an excellent fit for almost any the major oil companies. Devons proven reserves represent approximately 18% of the average Majors reserves, and 40% of them are oil. The company trades at $68 per share, but I believe Devon could be worth as much as $86 a share to a Major.

Occidental Petroleum (NYSE: OXY) is my third most likely buyout candidate. It has a larger international presence than either Anadarko or Devon, which could make it more attractive to a company like Royal Dutch Shell or British Petroleum. Oxy holds significant undeveloped reserves in Latin America (5.3 million acres), the Middle East (1.4 million acres), Russia and Asia (6.9 million acres). The company also has a legacy position in Libya, which has over 32 million acres of oil rich prospects. Occidental also has tremendous U.S. assets, including a strong position in the Permian Basin and a former strategic naval petroleum reserve in California. All of these assets provide Occidental or an acquirer with significant room to grow.

One of Occidentals strengths is its ability to find oil and gas cheaply. Over the last three years, the companys average finding cost was $5 per barrel. That was significantly lower than Exxons ($6), Anadarkos ($8.50), or Kerr-McGees ($17). In addition, Occidental Petroleum made a very savvy takeover bid for Vintage Petroleum. Oxy bought 437 million barrels of reserves for $8 per barrel. We will not see companies selling that cheaply in todays market. If Occidental gets bought out, I could imagine the shares commanding a very nice premium to their current price. Its shares currently trade for $91 McDep Associates set the present value of Occidental Shares at $120, a 31% premium over present-day prices.

I am confident that Occidentals acreage and probable reserves will command the highest per proven reserve price of the three companies listed I have discussed. However, I would advise individual investors to pay no more than $96 per share. It will be very interesting to see which of these three independent oil companies are still independent one year from now!

Link here (scroll down to piece by Matt Badiali).U.S. DOLLAR RECOVERS Why?

The brutal beating that the dollar has taken this week started this past Sunday, before the European and the U.S. forex markets even opened. By Monday evening, the USD lost almost 200 pips to the euro. But the buck got a break in Tuesdays overnight session, and Tuesday morning (Jan. 24), the press was full of headlines like this one: Dollar recovers as oil, stocks stabilize. You know, just once, I would like to see these experts actually trade forex based on the opinions they offer. Would they really go long the dollar every time crude oil falls? Would they really short the EURUSD every time the Dow rallies? They are so convinced of these presumed relationships among the markets, it would be great to watch the markets prove them wrong.

See, the beauty of this so-called analysis is that it can explain the markets movement in either direction. It is all about how you interpret the news and which stories you choose. On any given day, the news is a mixed bag. So, when the USD is up, you focus on stories that in theory could have moved it higher. And when it is down, you disregard the bullish fundamentals and only talk about the ones that could explain the markets downturn. The problem is, these experts are not really helping anybody. The careful selection of the news stories and the ambiguity that comes with it only make your trading decisions harder.

You want to know what really helped the dollar recover today? Market psychology. In Elliott wave terms, Tuesdays EURUSD decline was a fourth wave correction.

Link here.GROUNDBREAKING OVER SOME VERY OLD GROUND

It is hard enough to resist greed and fear when you are all alone and no one is watching. Heaven help the man in a crowd who tries to stand as an individual, once that crowd begins to act on its collective emotion. This is why discipline is usually the first word out of the mouths of consistently successful investors and traders, when they are asked how they managed to succeed. They know that while the market is a formidable foe, undisciplined investors face a far more lethal enemy namely their own emotions, and the emotional impulse to follow others. Decades of stock market history prove this to be true. Long-term peaks bring in the greatest number of people, even as long-term lows bring in the fewest. They buy high and sell low again, and again, and again.

Mountains of hard evidence notwithstanding, it is still common to see some academic get good press for conducting a groundbreaking experiment in crowd behavior. To wit, the recent piece on the ABC News Primetime show, which demonstrated the test results of a professor of psychiatry at a prestigious university in Atlanta. Here is the short version. A group of people takes a test together, with each person privately writing the answers. Then, the same group takes a similar test, though each person reads their answers aloud to the group. The outcome? Hearing the answers of others profoundly altered the test results. Many individuals would get high scores on the written test, only to get low scores on the verbal test after hearing the answers of others.

Each person in the group was also hooked up to a machine that measures brain activity. The one interesting (if not surprising) revelation was the brain activity of people whose verbal test scores were not influenced by the answers of others their brains lit up in the amygdala, which is the fear center of the brain. In other words, going against the group raised the fear level in these individuals, but they were disciplined enough to make independent (and rational) decisions. As I said, none of this is surprising this one test in an artificial environment is a weak echo of what real-world markets have long proven.

Elliott wave analysis cannot infuse discipline, but it can help you recognize patterns in the market particularly the highs, lows, and dominant trends that reveal the collective emotions of others. It can be the first step toward recognizing those emotions, instead of participating in them.

Link here.A LOOK AHEAD TO 2006 FROM BOB PRECHTER

Why was 2005 not a good year to be in stocks? Bob Prechter: The Dow was down slightly (0.6%) on the year. In 2005 investors holding Treasury bills and notes beat the Dow; they also matched the S&P and even the vaunted Russell 2000 Small-Cap index, which edged up 3% and paid measly dividends of 1-2%. What is more, we did it with no risk, while the masses who are still invested in the stock market are taking risk of historic proportion.

Are we headed up or down in the markets in 2006? The failure of the promise of a huge advance in the 5 year of the decade last year must have frustrated the bulls. On the other hand, it is frustrating for us waiting for this interminable bear-market rally to end. I expect 2006 to be another down year for the Dow, but this time

What signs do you see to support your bearish outlook? Society is reflecting a bear market in many respects: (1) The #1 movie of the past weekend was (another) torture film. (2) GM is slashing prices on most models. (3) New borrowing by the federal government has soared from a negative rate (i.e., net debt retirement) at the market top in 1999 to an all-time record. (4) Political scandal is ripening in Washington, for both Congress and the president. (5) Anti-immigration and protectionist forces are on the rise. (6) Anti-Americanism is rising in South America, where Bolivias recently elected president has created an anti-U.S. coalition with Venezuela and Cuba. (7) Womens fashions are becoming more conservative, with longer skirts, midriffs going back under wraps and darker colors. (8) Trade talks are breaking down. (9) Race riots are breaking out in France and Australia. I regard these events as compatible with the Elliott wave case that the advance of the past three years in the major averages has been a bear-market rally, not a new bull market. When prices decide to catch up to such feelings, all reflectors of social mood will be in gear on the downside.

Link here.WHEN HOT WOMEN PICK HOT STOCKS

Do celebrities pick stocks better than you? Or, a more alarming question, do they pick stocks better than the pros? Since 2003, Wayne Rogers, who played Trapper John on M*A*S*H, has been appearing on Fox News Channels Cashin In. Last September, Lenny Dykstra, the former outfielder for the New York Mets and Philadelphia Phillies, began writing a column for TheStreet.com. TheStreet.com has also signed up professional wrestler John Bradshaw Layfield to dispense investment advice. Playboy and Tradingmarkets.com are running a stock-picking contest in which 10 hot women pick five hot stocks apiece. Whoever is up the most at the end of the year gets $50,000 to donate to the charity of her choice. The leader so far is Amy McCarthy, the sister of Jenny McCarthy.

In general, these celebrity stock pickers take themselves seriously and offer sober advice. Rogers, a Princeton graduate, has a financial advisory firm, Wayne Rogers & Company. On Cashin In, he offers levelheaded thoughts generally indistinguishable from those offered by journalists, money managers, and investors on the program. On Jan. 16, his three recommendations were very conservative: Conseco, an insurance company; Leucadia National, a conglomerate run by savvy value investors; and cash. Lenny Dykstra looks for stocks whose return on equity is higher than the forward price-to-earnings ratio and that have lots of free cash flow and low debt. When the markets were tanking last Friday, he coolly recommended going deep on options of blue chips like GE.

The real, um, revelation has been McCarthy and her fellow Playmates. Last Saturday, the Wall Street Journal noted with astonishment that Amy McCarthy was up more than 20% through Thursday, January 19, beating every single one of the more than 6,000 mutual funds tracked by Morningstar. McCarthy did not do much research and chose five volatile small-cap stocks with very low prices. This is clearly a case of random choices beating the market. But McCarthy is not the only of the 10 topless women who is topping the market. The Journal noted that through Friday, the models have clocked a 3.41% average return, compared with 1.06% for the Standard & Poors 500. Deanna Brooks is up more than 8%, e.g. The thumbnail rationales Brooks gives for her stock picks are not that much different from the thumbnail rationales offered every day in outlets like the Journal and Barrons although this says less about Brooks stock-picking savvy than it says about the shallowness of the professionals analyses.

The competent celebrity results suggest how the markets have, in some ways, become more efficient as they have become more democratized. If you removed the bylines from the musings of Dykstra and Rogers and laid them alongside comments made by six random mutual-fund managers, you would not notice much of a difference. The lingo and methodology surrounding mainstream stock management have diffused everywhere stocks are bought. Pros and amateurs have the same raps and the same investment theses. Which is one of the reasons it is increasingly difficult for professional money managers even the putatively brilliant hedge-fund wizards to beat the market.

Or maybe it is not just luck. Maybe working in performance-related industries like athletics and acting can be an advantage to managing money. Take Lenny Dykstra. In Michael Lewiss Moneyball, Oakland As general manager Billy Beane mused about his former minor league teammate. Lenny was so perfectly designed, emotionally, to play the game of baseball, said Billy. He was able to instantly forget any failure and draw strength from every success. He had no concept of failure. And he had no idea of where he was. As a player, Dykstra was a hard-working guy who would thump his chest every time he scored and ignore every strikeout in other words, he had the perfect mindset for trading.

I cannot decide if the celebrity stock-picking trend is a dismal throwback or a refreshing tonic. On the one hand, one of the worst notions of the 90s boom was that you did not have to be a professional, experienced, or informed investor in order to make market-beating stock picks. The celebrity pickers hearken back to that age of amateur folly. On the other hand, the pendulum may have swung too far in the other direction. The celebrities puncture one of the biggest canards of the current decade that only highly paid investment professionals who spend their entire lives obsessing about the markets every move can easily beat it.

Link here.WHY WALL STREET HAD A RECORD YEAR AND YOU DID NOT

Securities firms in New York gave out $21.5 billion in end-of-year bonuses, according to the state comptrollers office. That is $125,500 per employee (although of course the money was not distributed anywhere near evenly). The last time things were this good for Wall Streets traders and bankers, at the end of the Internet boom in 2000, the rest of the country got to share in the fun. In 2005, by contrast, the S&P 500 had a total return of only 4.9%. Wage and salary growth for most Americans lagged inflation. So how is it that almost all of the big investment banks managed to have their best year ever?

One possibility is that Wall Street is a leech upon the body economic, sucking out the lifeblood of domestic industry and excreting it as Lamborghinis and $20 million Manhattan apartments for a lucky few. This is a theory with venerable populist roots, and it has undergone a renaissance lately. But even if you sympathize with that view, there remains the question of how Wall Street firms are able to get away with such behavior. If the big investment banks are earning unwarranted profits, wont competitors arise? Wont customers demand a better deal? And will shareholders not demand that the firms stop paying out half their revenues as employee compensation?

First, the competition: It can be fierce in certain segments of the securities business. But the fees paid for investment banking services reflect a very limited competition. And while banking revenues are highest when markets are booming, the current disconnect between rising profits and plodding stock prices has been driving CEOs to action. Whether they opt for an acquisition, a private-equity buyout, or a Tyco-style dismemberment, Wall Street gets paid. What is more, the big American investment banks are dominant overseas as well.

But fees for M&A and underwriting are actually no longer what drives the business. The big money now comes from trading. Much of the profit (just how much is not disclosed) is generated by traders executing tasks for clients making block trades, structuring derivatives contracts, buying currency for overseas deals, etc. Why is this so lucrative? It is partly a fair reward for taking risks, partly a byproduct of the knowledge the big firms accrue by being at the center of everything that goes on in global financial markets. They are profiting from their customers comparative lack of knowledge. How long will customers put up with it? As long as they lack knowledge, one presumes.

Yeah, the bonuses seem absurd. They are certain to come crashing to earth. At least, that is what Fortune predicted in a cover story in 1986 when the average bonus was $13,950. We are not going to make that mistake again.

Link here.HEDGE FUNDS EXPECT MORE DEFAULTS

Hedge funds and other investors in North American distressed debt are hoping to benefit from a rise in corporate default rates but think the increase in 2007 will be more dramatic than in 2006, according to a new survey. But the specialists in troubled companies, sometimes known as vulture investors, are cautious on bond valuations, preferring loans secured on specific assets over unsecured bonds in 2006. Among hedge fund strategies centred on North American markets, distressed debt investing was among the most successful last year, returning almost 10 per cent, according to the Hennessee Group. More than two-thirds of respondents said junk-rated companies would find it harder to refinance debt this year than last, potentially creating more opportunities for distressed debt specialists.

Not surprisingly, 84% of those surveyed expected to see fresh action in the automotive sector, where parts suppliers as well as carmakers Ford and GM themselves remain under pressure. Other sectors of particular interest were packaging, where rising energy and raw materials costs have squeezed margins, and healthcare and pharmaceuticals. Vulture investors can take heart from the past years trends in new issue quality, says Martin Fridson, publisher of Distressed Debt Investor. A robust supply of future defaults appears well assured. The new survey bears that out, with most respondents anticipating the high-yield default rate would rise from last years level of about 2% towards 4% this year with a sharper move above 4% in 2007.

Link here.INDIANA SELLS ROAD FOR BILLIONS; PREPARE FOR DELUGE

On Monday, Indiana Governor Mitch Daniels said a Spanish-Australian consortium had bid $3.85 billion to run the Indiana Toll Road, a 157-mile highway across northern Indiana that runs from the Illinois to Ohio, for 75 years. The legislature still has to approve the proposal, of course, but they are not going it alone with this concept. Indiana lawmakers have only to look north, to Illinois, for another example of how this kind of thing works. Last year, Chicago got $1.8 billion for its Skyway, a 7.8-mile long elevated highway that connects the Dan Ryan Expressway with the Indiana Toll Road. Lots of public officials took notice.

A Merrill Lynch report published last July on the subject of U.S. toll road privatization asked whether sales like the Skyway were one-offs, or do they represent the beginning of a sweeping trend that will spread to other tolled bridges, tunnels, expressways and long-distance toll roads? Bet on the sweeping trend. The money is just too big to resist, and the business of running toll roads just too marginal to what state governments are all about. Now that Illinois and Indiana have done it, look for other states to dive right in.

Merrill Lynch estimates that at least 18 states from California to Massachusetts have state-, county-, or city-owned toll roads that might lend themselves to privatization. In fact, there are probably candidates in almost all 50 states. What you need is an established road, and the flexibility to increase tolls. Do not underestimate the importance of Indiana, rather than, say, New Jersey, doing this, either. Indiana is one of the Republican-dominated red states, and one with a reputation for fiscal rectitude.

Link here.INDIA MAKES BERNANKES JOB AT FED LOOK EASY

Y.V. Reddy has not admitted he risks losing control of Indias economy. Nor does the central bank governor need to; markets are doing it for him. Indias bonds had their biggest plunge in seven months yesterday after Reddy unexpectedly raised short-term rates. It is not additional rate hikes that traders fear it is that rapid growth will fuel inflation. The Reserve Bank of India was right to raise its overnight borrowing rate to a three-year high of 5.5% from 5.25%. Its fourth increase in 15 months proved two things. One, Reddy is not in the pocket of politicians hoping he would stop boosting rates. Two, inflation is a bigger threat than many in the markets appreciate.

By raising its growth forecast for the fiscal year ending March 31 to 8% from 7.5%, the central bank effectively admitted its rate increases are not working. Reddy remains on the case, though. In a region in which many central banks are holding borrowing costs too low, India is throwing down the gauntlet. Reddys balancing act is a particularly dicey one that makes the U.S. Federal Reserves job seem like a breeze. Neither Ben Bernanke who succeeds Alan Greenspan as Fed chairman on Jan. 31 nor Jean-Claude Trichet at the European Central Bank, is juggling crushing poverty, wholesale-price inflation rising about 4.25%, high levels of foreign currency debt and credit-rating companies constantly looking over policy makers shoulders.

Link here.CHINA TO EASE FOREIGN EXCHANGE ACCUMULATION

China is committed to slower foreign exchange reserve accumulation, Zhou Xiaochuan, the governor of the Peoples Bank of China told the World Economic Forum, in rare comments about Chinas exchange rate policy. Mr. Zhou said that his country was committed to increasing domestic demand, rebalancing the economy gradually away from net exports, promoting consumption, particularly in rural areas, all of which would reduce the pressure on the country to keep increasing the rate of reserve accumulation at an annual rate of $200bn a year. We need to make a change to stabilize the [foreign exchange reserve] situation, he said. China has no intention of faster acceleration of foreign exchange reserves, he said, adding that he believed the pace of foreign exchange reserves will be reduced. But he damped hopes that China was on the verge of another, more substantial, currency revaluation.

China has been forced to accumulate $400 billion in foreign exchange reserves in 2004 and 2005 to stop the renmimbi from appreciating against the U.S. dollar and other leading currencies, bringing Chinas total reserves above $800 billion by the end of last year. That figure is on par with Japans reserves. Since it is believed that the majority of Chinas reserves are denominated in U.S. dollars, any revaluation of the renmimbi would impose large financial losses on Chinese people. The concern that Chinas investment in U.S. assets has left the country exposed to currency movements is likely to be one of the reasons for Mr. Zhous desire to slow further reserve accumulation.

Link here.EUROPES ECONOMIC SPRING

Start preparing now for increasingly favorable fundamental numbers to come out [of Europe] in the next several months. Elliott Wave Internationals European Financial Forecast, April 2005.

Every month, Ifo Institute for Economic Research in Munich publishes the latest readings of the German business confidence index. Germany is Europes largest economy, and this all-important index is viewed as a key gauge of the EUs overall economic health. It was in October 2005 when European economists first got a chance to let out the breath they had been holding for so long: That month, the Ifo index jumped to a 5-year high. It stayed upbeat since then, and this January, to analysts surprise, German business confidence climbed even higher to levels not seen since May 2000.

Meanwhile, German investor confidence is hovering near a 2-year peak, unemployment is improving, the economy has been gaining momentum since the middle of last year, and other EU nations are showing signs of faster growth, too. And here are just some of the ways analysts describe the current business climate in Europe: German business leaders, who were still ridden by angst last spring, now seem to be almost dancing in the streets, and There is a definite sense of economic spring in the air in Germany.

Well, the increasingly favorable fundamentals we predicted for Europe almost a year ago sure have arrived. But before you start to wonder how we knew to expect this recovery, read the rest of that April 2005 quote: Unfortunately, these lagging indicators will likely capture the attention of most analysts, and they will ignore the new information that the stock market will be offering. Um, unfortunately, we seem to have nailed this prediction, too. Because save for a few skeptics, European economists believe wholeheartedly that the upbeat economic numbers should be a massive confidence boost to recovery expectations. Confidence begets confidence, in other words.

Looks like a perfect time to put your cash to work in European stocks, does it not? Without a doubt, thats what most financial advisors would recommend you do right now, if not sooner. Except notice the words lagging indicators in our April 2005 forecast. Lagging, because most economic indicators lag the stock market. Stocks lead the economy, as the sequence of events in Europe over the past year clearly proves. That is why you cannot expect Europes economic spring to boost European stocks it works the other way around! Which is something conventional economists have no idea about.

Our European Financial Forecast turned bullish on Europe in September 2004, and it was not the good fundamentals that did it. No, the fundamentals were horrible at the time but Elliott wave patterns in European stocks were decidedly bullish. Dont expect Europes economic spring to tell you if stocks can continue their advances keep an eye on wave patterns instead. They are offering loads of new information right now.

Link here.WHAT ABOUT PALLADIUM?

When you think about precious metals, what elements come to mind? To be sure, gold, silver, and platinum come to the forefront. What about palladium? It is a precious metal, a platinum group metal, and a noble metal. Palladium was discovered by the British chemist William Hyde Wollaston in 1803. Few people have heard of this precious metal in spite of its myriad uses, a couple of headline-grabbing stories, and what may be quite an interesting future as to helping us break free of our petroleum-energy dependence perhaps even interesting enough to buy a few ounces for your portfolio.

Palladium is predominantly mined in Canada, Russia, South Africa, and the U.S. (Montana). To give you an idea of how rare this metal is, about 6.8 million ounces of palladium were mined in 2004. This compares to 79.2 million ounces of gold and 620 million ounces of silver mined in the same year. Platinum is slightly rarer with 6.4 million ounces produced in 2004.

Before delving further into the metal, I would be remiss not to mention a bullish contrarian indicator as to why precious metals are in the early stages of a bull market. As a surety bond underwriter, I analyze hundreds of personal financial statements every year. Bar none, real estate is where most people are investing their money. Equities (i.e., publicly traded stocks) come in a distant second place. Cash and bonds, of course, commonly occupy the asset side of a personal balance sheet as well. When it comes to precious metals, however, this asset class is completely off the radar screen. Maybe one in every 200 personal financial statements will list precious metals (mostly gold and silver) as an asset. So when you hear the talking heads say gold and silver have had a nice run but the party is over do not believe it. When the common man comes to realize that the Federal Reserve is debasing the dollar at breakneck speed, he is going to jump into precious metals with a vengeance. This is when the real fireworks will begin. We are not even close to this point yet and that is why I am bullish on precious metals.

Such like silver, palladium is a precious metal whose demand is derived chiefly from industrial users. It is a versatile metal, which is ductile and is resistant to both oxidation and high temperature corrosion. Notable applications include automobile catalytic converters, dentistry, electronics, fine instruments, jewelry, petroleum refining, and photography. On March 23, 1989, palladium became an integral part of headline news around the world. For on this date, at a news conference, Stanley Pons and Martin Fleischmann (both of the University of Utah) reported experimental results in which energy was generated via a cold fusion process. Pons and Fleischmanns apparatus essentially consisted of an electrolysis cell containing heavy water (dideuterium oxide) and a palladium cathode which rapidly absorbed the deuterium produced during electrolysis. What Pons and Fleischmann found was that the devices energy output exceeded the energy input. In other words, they had discovered a process to bring about nuclear fusion at room temperature or so they believed.

Similar experiments, conducted soon thereafter, produced disappointing results. Hence, a Department of Energy panel concluded: Nuclear fusion at room temperature, of the type discussed in this report, would be contrary to all understanding gained of nuclear reactions in the last half century; it would require the invention of an entirely new nuclear process. Alas, palladium had its day in the sun as a miracle metal that could safely bring us nuclear energy at a very low cost. For those who still believe, keep in mind that unexplained experimental results do not mean that Pons and Fleischmanns experiment was wrong. Superconductivity, after all, was first observed in 1911 and explained theoretically decades later in 1957. There is mounting evidence that Pons and Fleischmann were on to something big.

A fuel cell operates very much like a battery given that it produces power in the form of electricity. Unlike a battery, it does not run down or need recharging because it produces energy as long as fuel is supplied to it. Hydrogen-rich fuels, that have been successfully utilized, include biodiesel, diesel, ethanol, kerosene, methane, methanol, natural gas, propane, and others. If fuel cell technology becomes commercially viable, then the internal combustion engine will be replaced by fuel cells and the global dependence on petroleum as an energy source will diminish markedly. Fuel cells perform best when the hydrogen fuel is free of impurities. This is where palladium shines. Using a palladium membrane hydrogen purifier, pressurized hydrogen is diffused across the palladium membrane keep in mind that only hydrogen possesses the ability to diffuse through palladium. Once the hydrogen gas passes through the palladium membrane, an ultra-pure hydrogen gas may be fed into the fuel cell thus preventing the anode catalyst, in the fuel cell, from being poisoned by trace impurities. There are fuel cell manufacturers using palladium for this exact purpose.

Fuel cell power systems are already in use. They are being employed in hospitals, hotels, nursing homes, office buildings, schools, utility power plants, and an airport terminal either providing primary or backup power. Likewise, they are being used as primary and backup power sources in homes. It is also quite exciting that DaimlerChrysler, Ford, General Motors, Honda, Nissan, and Toyota each have working fuel cell powered cars. Optimists claim that fuel cell powered cars might be commercially available by 2010. As fuel cell technology progresses, the day may come where we are weaned off of our petroleum dependence. In turn, conceivably, a more peaceful world will emerge. And with palladiums future intertwined with the fuel cell, maybe we can make a buck or two by purchasing a few ounces of this hard-working precious metal. At $273 an ounce, palladium may be a bargain today.

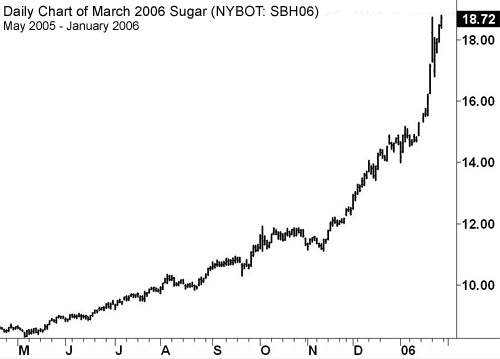

Link here.SUGAR EXPLOSION

Take a look at the sugar trend for the last year (chart here). Sugar is one of those markets that can rocket on a whim. Veteran traders will easily recall the years when markets like Sugar or Coffee or Cocoa traded substantially higher or lower the big trends out of nowhere. Often sparked by an assortment of third world concerns, these markets have a tendency to produce large trends in a short period of time.

Sugar has recently exploded to highs not seen in more than a decade. But how could you have taken advantage of a move like this? How could you have been ready for the next world event to shoot sugar to the moon? You need to trade with rules. You need to have a system. You need to be ready, with a market like sugar on your watch list, ready to enter on breakouts as it is making new highs or lows. You have no idea when you enter if it will go to the moon, but you still need to have a method that will get you in to be on board so if it does rocket up you do not miss it.

This Sugar move is even more proof of the theorem that trend following exploits worldwide events. Trend followers had ample time to position in Sugar while it was trading around 8.00 long before the market blew through 12, 14 or even 18. What technical signal would not have had you squarely into the Sugar trend? Trend following entry into the Sugar happened long before Brazil began to emphasize more and more sugar to make more Ethanol. However, the fundamentals did not matter if you were trading to take advantage of this incredible move. Traders who waited on the fundamentals to explain the rationale for the Sugar trade missed the initial breakout, and the big profits that resulted. Why do people have such a hard time just accepting the sugar trend (or any other trend) and just riding it? Why do people feel the need to explain why the move happened?

Link here.READY FOR $262 PER BARREL OIL?

Be afraid. Be very afraid. That is the message from two of the worlds most successful investors on the topic of high oil prices. One of them, Hermitage Capitals Bill Browder, has outlined six scenarios that could take oil up to a downright terrifying $262 a barrel. The other, billionaire investor George Soros, would not make any specific predictions about prices. But as a legendary commodities player, it is worth paying heed to the words of the man who once took on the Bank of England and won. Im very worried about the supply-demand balance, which is very tight, Soros says. U.S. power and influence has declined precipitously because of Iraq and the war on terror and that creates an incentive for anyone who wants to make trouble to go ahead and make it. As an example, Soros pointed to the regime in Iran, which is heading towards a confrontation with the West over its nuclear power program and does not show any signs of compromising. Iran is on a collision course and I have a difficulty seeing how such a collision can be avoided, he says.

Another emboldened troublemaker is Russian president Vladimir Putin, Soros said, citing Putins recent decision to briefly shut the supply of natural gas to Ukraine. The only bit of optimism Soros could offer was that the next 12 months would be most dangerous in terms of any price shocks, because beginning in 2007 he predicts new oil supplies will come online. Hermitages Bill Browder does not yet have the stature of George Soros. But his $4 billion Moscow-based Hermitage fund rose 81.5% last year and is up a whopping 1780% since its inception a decade ago. A veteran of Salomon Bros. and Boston Consulting Group, the 41-year old Browder has been especially successful because of his contrarian take; for example, he continued to invest in Russia when others fled following the Kremlins assault on Yukos.

To come up with some likely scenarios in the event of an international crisis, his team performed what is known as a regression analysis, extrapolating the numbers from past oil shocks and then using them to calculate what might happen when the supply from an oil-producing country was cut off in six different situations. The fall of the House of Saud seems the most far-fetched of the six possibilities, and it is the one that generates that $262 a barrel.

More realistic and therefore more chilling would be the scenario where Iran declares an oil embargo a la OPEC in 1973, which Browder thinks could cause oil to double to $131 a barrel. Other outcomes include an embargo by Venezuelan strongman Hugo Chavez ($111 a barrel), civil war in Nigeria ($98 a barrel), unrest and violence in Algeria ($79 a barrel) and major attacks on infrastructure by the insurgency in Iraq ($88 a barrel). Regressions analysis may be mathematical but it is an art, not a science. And some of these scenarios are quite dubious, like Venezuela shutting the spigot.

OPEC Acting Secretary General Mohammed Barkindo said OPEC will step in at any time there is a shortage in the market. But then no one in the industry, including Van der Veer, foresaw an extended run of $65 oil or even $55 oil like we have been having. It is clear that there is very, very little wiggle room, and that most consumers, including those in the U.S., have acceded so far to the new reality of $60 or even $70 oil. And as Soros points out, the White House has its hands full in Iraq and elsewhere.

Link here.MAYBE ITS DIFFERENT THIS TIME